Over the past month, Berkshire’s cash has risen to over $320 billion, more than double the previous high in nominal terms and as a percentage of total assets. Buffett and his coterie of exceptional managers are witnessing unprecedented stock market shifts that are more alarming than ever.

Current geopolitical and economic factors contribute to the stock market’s extremity and potential volatility. This article dives deep into the factors likely leading to historic market declines and a significant pivot in the world order.

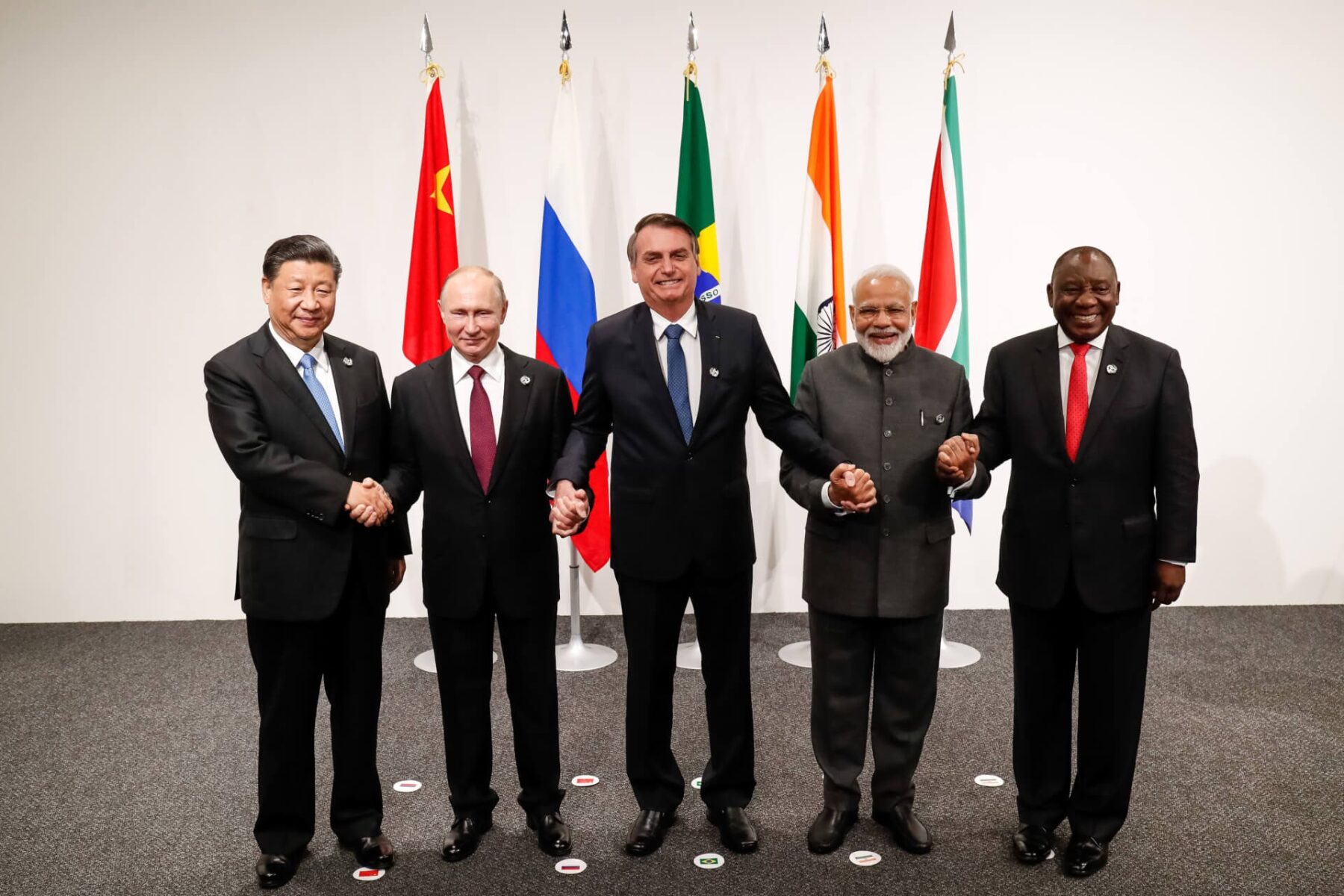

While the coalescing of BRICS+ (originally Brazil, Russia, China, India, and South Africa) is part of the equation, there’s much more to the story.

For the record, BRICS+ is not an anti-Western bloc of nations – far from it! There’s a big difference between the definition of anti-Western and non-Western. BRICS+ is a non-Western cooperative bloc of nations seeking global economic growth, from which all share the benefits of global trade.

Trade between countries is a sign of prosperity, as exporting a nation’s goods contributes to its overall gross domestic product (GDP). The higher the GDP…, the higher the standard of living.

Meanwhile, if the Western bloc of nations (namely the G7) chooses to get on board and cooperate, it would benefit both the collective West and the global economy. Unfortunately, the lion’s share of the Western bloc has been unwilling to cooperate thus far. Uncooperative economic behavior will undoubtedly cause the Western bloc of nations (including the U.S.) to be eclipsed by the ubiquitous trade alliances of BRICS+ and the SCO Shanghai Cooperation Organization.

This perilous blind spot is foundational in the current economic problems the collective West is facing, especially the United States. These problems didn’t manifest last week; they’ve been building momentum over the past 50 years. Undeniably, these geopolitical and economic issues have now reached a critical mass where they can no longer be swept under the rug or ignored by citizens alike. The West has reached a point of inflection where “crashing and burning” is nearly a syllogistic economic outcome.

As daunting as this may be, there’s still hope. The United States ‘president-elect’ can implore Western acceptance of the glaringly obvious new world order. The West must be willing to extend a hand to join BRICS and the SCO. This alliance may not avert a catastrophe but would at least soften a crash landing. Let’s pray there’s still a seat at the table… before it’s too late!

The Fed’s On High Alert

The most visible warning sign that “trouble’s on the horizon” occurred when the Fed initiated a 50-basis point interest rate cut in September 2024. Consequently, this was rapidly followed by another 25-basis point cut in November. Take heed, and pay attention.

In the past, a meaningful decline in Fed Funds never led to a sharp upturn in longer-term interest rates for many reasons. First, lower short-term interest rates equate to ‘cheap money,’ and more cash floods the economy. Some of this floating cash returns into longer-term and higher-yielding securities. Second, when interest rates fall, this decline leads some companies and institutions to lengthen the maturity of their fixed-income assets to compensate for investors earning less income from their shorter-term holdings. Psychologically, when the Fed cuts interest rates, it reaffirms the Central Bank’s confidence that inflation is under control.

However, this time around, the reaction in longer bond yields was alarming. Simultaneously, long-term yields exploded as the yields on ten-year bonds climbed nearly 25% in the two months following the Fed’s pivot.

Folks, this is a sign that the Fed has lost control over the economy.

The Fed’s actions were designed to lower inflation and desperately needed cost reduction of essential goods. However, this never occurred. The Fed’s failure to tame inflation, disguised by skewed stats presented by the mainstream media, could only fool you for so long!

False Employment Reports

While bond yields cannot be hidden, the same is not true for many economic data, such as employment. For example, reported payroll employment has been showing solid growth; however, since the Pandemic waned, there’s mounting evidence that these numbers are not the whole story.

The Bureau of Labor Statistics admitted they overstated employment numbers by over 1 million workers during the past two years.

In reality, the employment growth rate is much less than originally reported. Moreover, other statistics representing the health of the labor market health are downright recessionary.

Measures of job availability have been steadily declining since the first quarter of 2022. A staggering 40% of current labor market stats are on par with the 2008- 2009 recession and way worse than the “dot.com bust” stock market crash in the early 2000s.

Let me be clear: evidence to reinforce the economy is much weaker than reported comes from small and medium-sized businesses (SMEs). This broad sector represents about 45% of economic activity and 55% of job creation. Surveys of SMEs date back to the mid-1970s. The SME Index has been well below historical averages over the past three years. This is bad news, folks.

Most striking, small business uncertainty recently hit an all-time high, consistent with recessionary conditions rather than solid economic growth.

Furthermore, the gross economic data reveals nothing about the enormous economic inequalities. Our conservative calculations estimated that less than 40% of the country had enough income to afford the necessities of life. For example, the Economic Policy Institute estimates less than 10% of the population in America can afford a decent standard of living.

Who’s To Blame?

Federal Reserve has a macro view of the actual economic situation in the United States. Despite the putative strong economy, the Fed acted too late in response to the mounting rise of inflation they had previously deemed transitory. Once the writing was on the wall and inflation was here to stay, the Fed reacted dramatically, rapidly raising interest rates.

How did the U.S. end up in this terrible economic situation?

Well, over the past decade, interest rates have been historically low. The Fed underestimated the inevitable inflationary impact this would have on the economy. But this is just the tip of the iceberg – merely a consequence of the underlying causes.

The strongest sign that Powell and Buffett had erred in their thoughts was the stock market. The stock market is typically the strongest sign the economy is performing well… or is it? There’s an old saying:

“Markets climb a wall of worry”

Modern Translation: Markets rise in anticipation of the Fed ameliorating these worries by increasing economic liquidity. However, over the past 15 months, a substantial 50% rise in the S&P 500 suggests abundant liquidity already exists in the economy!

This might tempt you to say that the Fed caused a strong case of stagflation – strong inflationary pressure combined with poor economic performance. Stagflation was a hallmark of the mid-70s to early 80s.

Again, whether it’s inflation, stagflation, or something in between, the consequences of today’s economic problems dwarf those of 1974. This was the year stagflation entered our vocabulary. By some measures, the stock market experienced a decline in 1974 nearly as horrific as the aftermath of the Great Stock Market Crash of 1929.

Are we seeing some parallels in today’s economy? Yes.

What does this mean to you?

Whether you’re an investor or simply curious about the state of the economy and overall financial well-being… drop a line and be sure to subscribe for future updates!